Charitable And Individual Gifting Considerations

If you are making charitable donations, the right moves could bring more benefits to the charity and to you.

To deduct charitable donations, your gift must go to a qualified charity or crowdsourcing campaign with a 501(c)(3) non-profit status. The I.R.S. needs to know three things: the name of the charity, the gifted amount, and the date of your gift. Ideally, the charity will provide you with proof of your contribution through a form but a receipt, a credit or debit card statement, a bank statement, or a cancelled check which includes that pertinent information will also work.1

To deduct charitable donations, your gift must go to a qualified charity or crowdsourcing campaign with a 501(c)(3) non-profit status. The I.R.S. needs to know three things: the name of the charity, the gifted amount, and the date of your gift. Ideally, the charity will provide you with proof of your contribution through a form but a receipt, a credit or debit card statement, a bank statement, or a cancelled check which includes that pertinent information will also work.1

Due Diligence: Sites like CharityNavigator.org, CharityWatch.org, or GiveWell.org can help you evaluate charities and learn how effectively they utilize donations. If you are considering a large donation, ask the charity involved how it will use your gift.

Maximize the impact of your gifts. Check with your employer - some companies match charitable contributions made by their employees. A charitable remainder trust or a contract between you and a charity could allow you to give away an asset to a 501(c)(3) organization while retaining a lifetime interest. You could provide a gift of life insurance or leave cash or appreciated property to a non-profit organization as a final contribution in your will.1

Donating an appreciated asset can be a tax-savvy move.

Highly appreciated securities: In higher income tax brackets, selling appreciated securities owned for more than a year can lead to capital gains taxes. Your letter of instruction to a bank or brokerage authorizing a transfer of shares to a charity can help you avoid paying the capital gains tax you would normally pay upon selling the shares, take a current-year tax deduction for their full fair market value, and the charity gets the full value of the shares, not their after-tax net value.2

Charitable IRA gifts: If you are wealthy enough to view the annual Required Minimum Distribution (RMD) from your traditional IRA as a bother, consider a qualified charitable distribution (QCD) from your IRA to satisfy some or all of your RMD; the amount gifted is excluded from your adjusted gross income for the year. 2

Life Insurance Policy: An irrevocable gift of a life insurance policy to a qualified charity can get you a current-year income tax deduction. If you keep paying the policy premiums, each payment becomes a deductible charitable donation up to the deduction limits. 3

Vehicle Donation: You probably will not get fair market value for the donation; if that bothers you, you could always try to sell the vehicle at fair market value yourself and gift the cash. As organizations that coordinate these gifts are notorious for taking big cuts, you may want to think twice about this idea.4

Making Cash Gifts to Individuals

Most of us will never face taxes related to money or assets we give away. In 2017, any taxpayer may gift up to $14,000 in cash to as many individuals as desired. Every taxpayer can gift up to $5.49 million during his or her lifetime without triggering the federal estate and gift tax exemption. The gifts may be made in cash, or they can be made in stock, contributions to 529 plans, collectibles, real estate – just about any form of property with value, as long as you cede ownership and control of it.5

The federal gift tax: The IRS sets annual and lifetime gift tax exclusion amounts, but few taxpayers or estates will ever have to pay it. Many people wrongly assume that if they give a gift exceeding the annual gift tax exclusion, their tax bill will go up next year as a result. Unless the gift is huge, that won’t likely occur. While you have to file a gift tax return if you make a gift larger than the annual individual limit, you owe no gift tax until your total gifts exceed the lifetime exclusion.5

The lifetime exclusion: If exceeded, you will pay a 40% gift tax on gifts above the current lifetime exclusion amount. One exception, is that gifts that you make to your spouse are tax-free provided he or she is a U.S. citizen. This is known as the marital deduction. Also, the gift tax and the estate tax are unified. If you have already made taxable lifetime gifts that have used up $3 million of the current 2017 unified limit of $5.49 million, then the remaining $2.49 million of your estate will be exempt from inheritance taxes if you die in 2017. If you don’t use all of it up during your lifetime, the unused portion of the credit can pass to your spouse at your death.5

Citations:

1 - www.desmoinesregister.com/story/money/business/columnists/2017/08/23/6-tips-making-smart-and-effective-charitable-donations

2 -irs.gov/retirement-plans/retirement-plans-faqs-regarding-iras-distributions-withdrawals

3 - kiplinger.com/article/taxes/T021-C032-S014-gifting-a-life-insurance-policy-to-a-charity.html

4 - pe.com/2017/11/04/its-not-that-hard-to-give-cash-or-stock-to-charity

5 - www.forbes.com/sites/deborahljacobs/2013/01/02/after-the-fiscal-cliff-deal-estate-and-gift-tax-explained

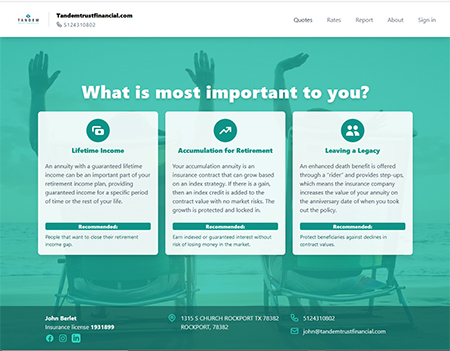

Annuity Guide

Learn more about the various annuity options available that can help you secure your retirement income.

DownloadTandem Trust Financial

John Berlet

(512) 650-2653 John.Berlet@RetirevoMail.com

Licensed in 33 states. John Berlet CA Ins Lic #0f06781, John Berlet TX Ins Lic #2609695

Social Security Guide

Learn about some of the strategies you can consider to maximize your Social Security benefit.

DownloadContact

Fill out the form below with your questions and for updates to our full library of retirement planning articles, videos, and downloadable booklets.

John Berlet

John.Berlet@RetirevoMail.com1315 S Church Street Rockport, TX 78382

(512) 650-2653Licensed in 33 states. John Berlet CA Ins Lic #0f06781, John Berlet TX Ins Lic #2609695

Visit my annuity specific site to learn more.